Thank you! Your submission has been received!

Oops! Something went wrong while submitting the form.

.svg)

To Our Partners:

I am writing to report on the 2025 season and all that the GLF team is doing to build a great business on your behalf.

In 2025, we began to see early positive momentum. Almond and pistachio price were both up 25-50 cents vs. 2024. In GLF LP, we had positive EBITDA for the first time as we ramped to mature and navigated low prices - largely thanks to dropping our breakeven Cost of Production (CoP) by 54 cents (12%). We have more debt than I’d like and are pre-paying to de-lever, so we are still Free Cash Flow negative. But we are moving in the right direction - and are hard at work to lower breakeven CoP further in 2026.

In our developments, Route 66 (AZ) and the OZ fund, we beat our budget on cash invested into the farms, i.e., we are building to a cheaper basis. Arizona’s young trees beat the UC Davis benchmark for the 3rd year in a row - showing again that the region can produce at California levels and deserves California values.

On a personal note, my son Liam finished treatment in the spring and is now scanning cancer free. Thank God! We also added our 5th, Matthew, to the clan.

Despite some positive updates, times are still tough. We are in the great recession of almonds - growers haven’t had it this hard since the 1980s. Peak acres and great weather in 2020, followed by extreme difficulty exporting via post-covid supply chains, extended and deepened the downcycle. We are still digging out 5 ½ years later. There have been many bankruptcies, many more abandoned orchards, and growers are at the end of their rope.

Vs. that peer set, we are ahead. Blended across our equity, our performance is at 0.95x vs. 0.74x for our benchmark, the NCREIF. Of course, with those marks, we’re not at all satisfied.

We can see the differentiation of our model: our returns are better; our cost of production is dropping; our profits are improving; and, thanks to you our partners, we are better capitalized (many growers stopped making payments years ago; GLF LP has never missed a covenant). Still, we aren’t celebrating being the fastest snail.

Building a business during a once per 50-year downturn has not been easy. We are working extremely hard through this moment, on your behalf (and ours - most of the team, myself included, has the vast majority of their net worth in GLF), and know we are getting better and better each day.

I was talking to another founder friend recently about working through tough moments and the mindset it takes. He runs a successful SaaS business. They have raised money, grown, and built a product that provides a lot of value for their customers. But suddenly, he finds himself in the "SaaSpocalypse." Because they are not AI-native, they are out in the cold. He is facing tough decisions and his team, his investors, and he and his cofounders are feeling the heat.

He shared the motto they’ve adopted: “this is when you earn it.” In other words, navigating the tough times is how you buy entry to the good times. Jeff Bezos has a similar quote: “When somebody congratulates Amazon on a good quarter…what I'm thinking to myself is— those quarterly results were pretty much fully baked about 3 years ago.” This year, I want to talk about that dynamic - earning it in the tough times. For us, that means believing at the bottom; harvesting advantage created years back; and continuing to invest now to produce results years into the future.

Earning it in the lows is especially true in commodities. The hard times are really, really hard. There is little to no profit, capital dries up, and sentiment is dire.

That can trick folks who aren’t as familiar with businesses like ours. It just doesn’t line up with pattern recognition from other sectors. In most businesses, good results precede great results - and bad results are a warning sign. In commodities, at the exact moment when you should be investing, the bottom, you look at companies’ results and think - geez, this is freaking brutal.

But that’s the trick - low prices solve low prices. Capital flees, supply dries up, and then price starts to rise. Eventually, price recovers, and those who stayed in benefit disproportionately.

I was at TPG in 2014, when oil price nearly halved after the shale boom. I remember hearing, from some of the world’s greatest investors, “I don’t think we should even be in energy. You just can’t make any money.” “We should bag it.” I would guess there were many Texas billionaires who happily disagreed with the prevailing PE sentiment.

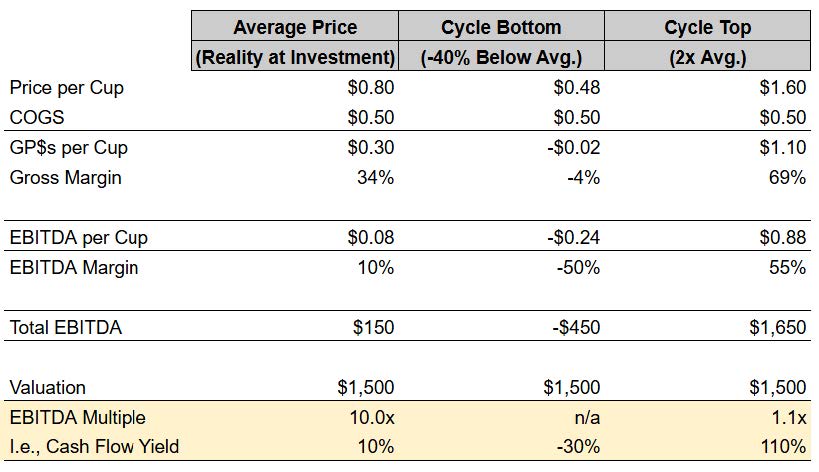

Why is believing at the bottom so hard? Let me illustrate by taking a non-commodity business and applying commodity economics. I’ll use one of my TPG companies, Chobani yogurt. Chobani when we invested was growing quickly and was the top Greek yogurt brand in the country. (They had some other short-term issues which I’ll ignore for simplicity.) When we invested, we thought we were buying $150Mish of EBITDA for about $1.5B, or 10x.1

Imagine though if Chobani were subject to commodity price swings. At cycle bottom, price might have slid 40% (same as what happened in almonds in 2020 or oil in 2014). On a $1.5B valuation, with downcycle price, Chobani would be earning -50% margins and -30% Cash-on-Cash (-$450M on $1.5B). Ouch.

But, at the top in commodities, price is often double the long-run average. Chobani with 2x its “average” price would make $1.65 - more than the $1.5B company value, or 110% Cash-on-Cash.

So - let’s say you were presented the opportunity to buy in at the bottom. If this was a normal business, you would run. But in commodities, you should think twice.

You have to look through that downcycle P&L to an average price one. And, keep in mind that typically, upcycles follow the downs - low prices dry up supply and cause high prices.

Savvy experts - from Texas oil families to the conservative, old-timer almond farmers, know not to be overly concerned at the bottom. They keep operating their best right on through. Believing in those moments when times are tough and it's hard to see through to the other side is the first step to earning it in the tough times.

The next piece of earning it at the bottom is reaping the rewards of past effort. For us, this shows up in our differentiation (primarily from lowering CoP) and diversification.

Another misunderstood aspect of commodity businesses is that folks think you can’t differentiate. But that’s not true. Just look at Saudi Arabian oil or even Costco - they build edge via their low cost and are extremely advantaged over the rest of the market. Since we started, we have been working hard to differentiate vs. other growers, too.

In 2022, we started a major overhaul of our farming team. Until that point, we frankly scaled the ops way too slowly. Starting in 2022-2023, we built a much stronger team; designed a system where most operating decisions get made by the guys at the farm every day; and then continuously reviewed our agronomic and financial results, to methodically, doggedly improve. A lot of credit goes to Jackie, Armando and our AMs and FMs who have been instrumental in taking us from a so-so to a good grower. Now, we are working hard to keep going from good to great.

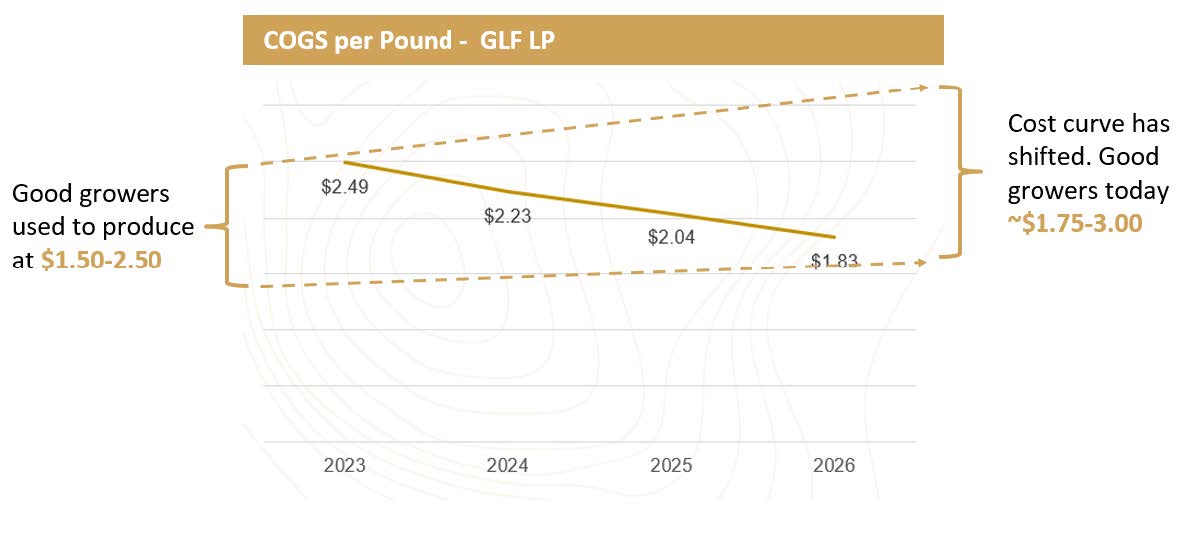

This work from 3-4 years ago is paying off today. Our industry has been through the ringer - even as price fell, growers’ costs have risen. Our costs have been flat. With growers strapped and underinvesting, industry yields in 2023-2025 were well below long-run averages. Our yields have increased every year. This drives our Cost of Production down, taking us closer to profits even as price sits below average. You can see below how we stack up on COGS per Pound2 over the last few years and where we think we can take the portfolio in 2026 below.

The tough calls we made to roll back some organic blocks, change out folks on the team, and constantly improve are paying off in our CoP and moving us down the cost curve, more and more competitive vs. other good growers.

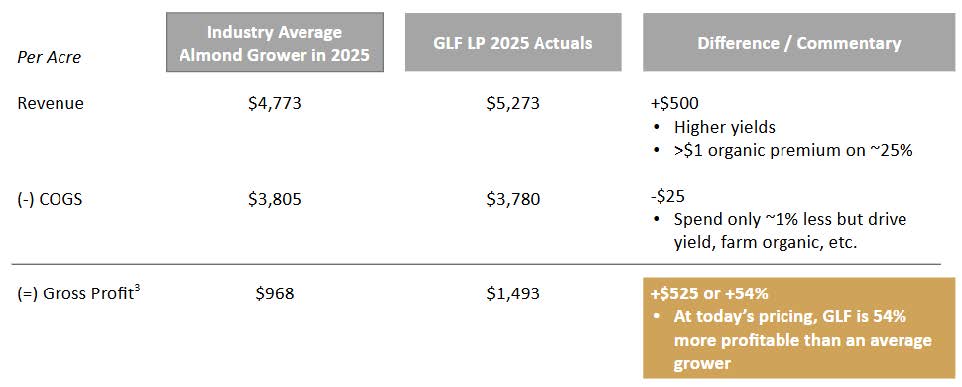

To state our differentiation differently, lower CoP means more farm profits. We have more revenue (from our yields and organic price), similar farming costs, and therefore, make more money at the farm level than the average grower.

Of course, we need to outperform - we operate a large, diversified portfolio that takes more overhead than a mom-and-pop grower. And we have expenses they don’t due to our investor backing.

Still, our farm-level edge is real and increasing with time. We will continue pushing in 2026.

Besides being differentiated vs. average growers, we are much more diversified. This is another place where investor-backing and scale pays. We are lucky to have nearly 6,000 acres, spread across the entire state (320 miles north to south, covering 80% of world supply), in one business at GLF LP. That is a result of the over 85% of you who voted to consolidate from SPVs into the new structure in 2023. (Thank you!) We are seeing this pay off in big ways today.

Few growers are our size. The ones that are typically farm in one single area. This can be good - they can operate out of one hub - but leaves them vulnerable to one of the biggest risks in farming - weather. This year, I looked at the performance of other large growers who are our size but concentrated in one place. For one, hot weather during harvest dropped results by half two years ago. For another, a spring freeze wiped their crop by more than half a year or two prior.

We are lucky to have the diversification we do - by region, water district, even crop (with almonds, organic almonds, and pistachios). It means less risk, more consistent performance, and taking advantage of the good in ag while partially shielding us from downsides other farmers must face.

So to earn it in the lows, you have to believe, you have to reap the rewards of past effort, and finally, you have to invest now to create payoffs for the future. We are working today on the next set of results that we expect to come through down the road. How are we doing that? Let me touch again on differentiation and diversification.

At average price and yield, we expect GLF LP to throw off steady-state EBITDA of $10-20M. But sometimes, we forget to factor in Route 66 and the OZ farms, which today are still largely immature. That represents about half our acres and could be worth another $20-30M of EBITDA at average price once they too are mature.

Though GLF LP felt the full force of the downturn, these developments were largely countercyclical. They did not produce much or any crop during the low price years. Investors in these funds are outperforming the benchmark, in Arizona by a wide margin. When online, these high quality orchards will produce a lot of cash.

The other thing about these orchards is that they will produce at a low cost of production. Already, the producing (but not yet mature) OZ almonds are at $1.86 COGS per pound. That is below GLF LP’s average, $2.04. In Arizona, our oldest block is 2 years from mature but already at $1.96.

We talk so much about GLF LP that it is easy to forget those assets (about half of our invested equity) are building in the background and will soon come to fruition. When they are ramped a few years down the line, investor cash flow and equity value will benefit from the work happening today. And our CoP will continue to drop - furthering our edge vs. the industry.

We are a large grower - probably a top 10-20 grower globally in our crops. Already, this has translated into earlier payment from our processors. This year, Jackie even lined up direct sales and minimum price guarantees, leading to higher prices for us vs. your typical farmer.

Going forward, we think our scale and strong, long-term processor relationships can diversify the business beyond being “just” a grower today. Processors need volume, but most growers are too small to matter - processors gather volume from many farmers. We are a meaningful free agent - our volume is split today over a half dozen very good processing partners. If we eventually commit our volume, we believe minority equity ownership (or similar sources of extra margin), may be on the table with little or no capital investment. This could be worth millions of dollars to investors and would create an incremental income stream that diversifies us from our farming profits today.

The team and I have embraced the tough times, and are working hard to “earn it.”

Today, this means quality farming to drive yields up, keep costs tight, and drop our breakeven CoP. It also means seeing through to the other side and buying in despite the downcycle. We appreciate that the vast majority of you get that too - adding equity in GLF LP/OZ and now Route 66, in effect taking the ball into our own hands to protect from skittish lenders and industry distress. We know these decisions are not easy, and we appreciate your partnership. We are co-investing our dollars, too, and matching that with tough calls (from layoffs to vendor negotiations to doing more with less), grit and hard work.

Our goal is not just to reach the other side of the cycle, though. Our aim has been and continues to be building a great business on your behalf. We are continuing to invest into that future today.

What might this look like? Down the line, as price recovers and AZ/OZ mature, we will hit positive EBITDA (this year in GLF LP) and then next, FCF. When we reach the other side, we will monetize via cash flow and potentially some asset sales, to reset our balance sheets and drive investor cash flow. We will continue to press our CoP edge as we aim to differentiate vs. other growers (via better people, better farms, better farming). And we will also further our edge vs. others in diversification (potentially by proposing a merger of AZ/OZ with GLF LP, eventually) to capture the good in ag and protect from its risks.

The team and I are bought in, proud to see some early positive momentum in 2025, and are not letting up. We appreciate your partnership and are looking forward to another year of building a great business on your behalf.

All the best to you and your families in 2026.

Jack